Can I Deduct Nanny Expenses on My Tax Return?

Can I Deduct Nanny Expenses on My Tax Return?

In a nation where nannies are one of the most fundamental parts of the working culture, it comes as no surprise that there are many laws specifically focused on them. Some of the most important ones, however, are the tax laws that guide people on how to deduct expenditures paid to these professionals. So, if you ever wondered; can I deduct nanny expenses on my tax return, the answer is generally yes. Figuring out the amount that you will be able to claim, on the other hand, takes a lot more effort. This is because everything from your income level to filing status has an accompanying limit that reduces eligible costs.

The Actual Numbers

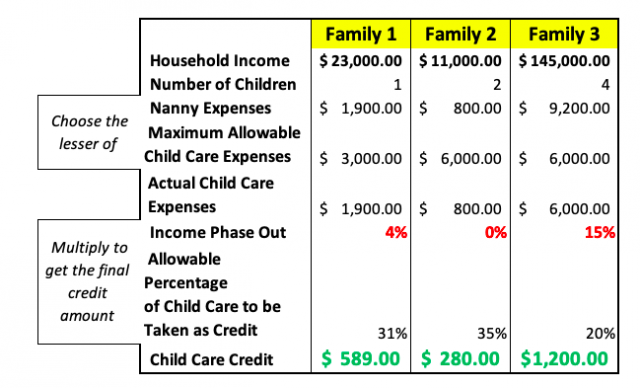

Prior to diving into the underlying process and legalities, let us look at some dollar figures pertinent to the credit. As of 2019, which accounts for the recent changes under the “Tax Cuts and Jobs Act,” you can deduct between 20% and 35% of up to $3,000 that you spent on your nanny for one child. If you had more than one child, regardless of how many more, the maximum that you can include is $6,000. The phase-out range goes from an income level of $15,000 to $43,000. More precisely, the IRS requires you to reduce the 35% by 1% for every $2,000 that your adjusted gross income exceeds $15,000. Once you hit 20%, you have reached the minimum of the allowable amount. Thus, the non-refundable credit for one child can range from $600 to $1,050 when the maximum $3,000 worth of expenses are used. To get a well-rounded idea, consider the following table.

Legal Requirements to Claim Nanny Expenses

The Internal Revenue Service, or the IRS, has a strict set of rules concerning if you can deduct deduct nanny expenses on your tax return. First, they refer to nanny expenses as “child and dependent care,” and those who are eligible can receive credit for it. That credit will be a dollar-for-dollar reduction of the final tax liability. So, if a married couple owes $4,600 for the prior year’s tax, a child and dependent care credit of $2,000 would bring that number down to $2,600.

Before getting into a deeper discussion about the credit, there is one important distinction that you should make. Child and dependent care credit is not the same thing as child credit. The latter applies to merely anyone who has a minor child or dependent. Your case is based on expenses that went toward getting appropriate care. If you never hired a nanny or enrolled your child in any type of daycare, you will not get to claim anything.

– Child Qualifications

For the child to qualify, they must be under the age of 13 during the time that the care was provided. Fortunately, the IRS will let you pro-rate the expenses in the year when your child exceeds the age threshold. For instance, if your son or daughter, who has a nanny that takes care of them whilst charging you $200 a month, turned 14 in September, you will still get to take eight months of the expenses into account. While the full amount would equal $2,400, you will lose $800 of it since the child was not 13 or under during the last four months of the year. Additionally, two other factor determine if you can deduct nanny expenses on your tax return; (1) your child cannot provide more than half of their financial support, and (2) they must live with you for more than half of the year.

– Why Did You Hire a Nanny?

The next question that you must answer is why you hired your nanny in the first place. This is because the government only lets you claim a care credit if your nanny was necessary for you to work or find work. When you hire someone to take care of your child because you simply want some time to relax, those expenses will not be eligible for the credit. One of the most common situations where people forget about this rule is when they try to deduct an occasional nanny expense they paid whenever they went to dinners. While you might have a great case for hiring someone to take care of your child as you and your spouse go on a date, per se, this is not a work-related expenditure.

– Who Was Your Nanny?

Because a lot of households outsource their nanny care to someone that they trust, it is not uncommon to see other family members step in. Paying them, however, does not immediately equate to a credit. Your nanny must pass a few tests related to their relationship with you, and the following examples would make them ineligible:

- Your nanny was one of your other dependents. This often happens when your parent lives with you.

- You let your other child take care of their younger sibling and give them an allowance in return.

- Your wife or husband took care of the child while you worked.

Each of those situations would mean that you cannot claim any expenses.

– Did You Earn Any Income?

Nanny expenses will not apply if you had no income during the year. Things that you would include in the calculation are salaries, tips, taxable compensation, and any net earnings from your businesses or self-employment ventures. What has no impact on your earning level, though, are pensions, annuities, interests, dividends, workers’ compensation, unemployment compensation, scholarships, social security benefits, and a few more. To obtain a full list, visit Publication 503 from the IRS.

– What Is Your Filing Status?

Finally, you have to take your tax filing status into account as well. Even though most folks who claim the credit are married filing jointly, there are cases where they also submit returns as heads of households or married filing separately. In a small number of cases, which occur when you are legally divorced, you may be able to get the credit when you file as a single taxpayer.

![]()

Reporting Childcare Expenses

All child or dependent care expenses go on Form 2441. It is a relatively simple form that consists of two pages and 31 lines. As with most other tax-related paperwork, you may not have to fill out every single line, and there is a good chance that you will need to transfer the final amount to another form. In this case, you would take the amounts from lines 11 and 28, which represents the credit and potential taxable benefits, to the lines 49 and one of your form 1040.

– What If You Do Not Know Your Nanny’s Sensitive Information?

If you ever looked at a form 2441, you probably noticed that the first part deals with details about the nanny or the organization that took care of the child. This is considered an expanded line one where you must put the name, the address, and the social security or the employer identification number of the caregiver. There are many situations where such information is not readily accessible. If you ended your relationship with a temporary nanny before collecting such information, for instance, you may find yourself struggling to get the necessary data.

Luckily, the IRS will still let you submit the form and claim eligible expenses. The only caveat is that you must prove that you did your due diligence when trying to collect the information. A few simple ways to do so is to showcase a scanned copy of the nanny’s invoice, W-4, or some other identification. Then, attach documentation showing that, while unsuccessfully, you at least attempted reaching out to the person or organization. Their failure to give you the data is going to open them up to liability as well, which is why most caregivers ensure that they stay compliant.

Do You Need to Issue a W-2 or 1099 to Your Nanny?

The IRS is quite firm in its belief that a nanny is a household employee, not an independent contractor. The reasoning behind it is the legal status of an employee. Unlike contractors, these individuals have to obey a certain schedule and handle a predetermined set of responsibilities. If a nanny was viewed as an independent contractor, they could take care of the child whenever they pleased, and they could do whatever they wanted when they provide their services. Given how practically all parents set certain expectations that overstep the role that they can have with contractors, treating your nanny as an employee is advised.

– Vacations, Workers’ Compensation, and Overtime Pay

Since you will technically reach the status of an employer, you should purchase some form of workers’ compensation insurance policy. Although it may be yet another expense that you have to account for, it can save you a lot of money in case your nanny suffers an injury while taking care of the child. The requirements surrounding vacation are a bit looser as you get to determine how many days off your full-time nanny gets.

The best way to go about the process is to simply communicate with the person that will be providing the service. Doing so helps you see what their expectations are, and you will get a chance to find some matching dates when your household may want to go on a vacation as well. Keep in mind that the better the vacation policy, the higher the quality of your applicants.

As far as overtime, you do need to pay overtime amounting to 1.5 times the normal rate to a nanny that works more than 40 hours a week. Courtesy of the Fair Labor Standards Act, failing to do so could expose you to enormous penalties.

Is Your Employer Providing a Dependent Care Benefit Plan?

To help people account for their childcare expenses and save on taxes, many employers offer dependent care benefit plans. These operate similarly to typical retirement plans as they are subtracted from the pre-tax income and the taxpayer gets to deduct them from taxable earnings. By contributing, you are putting your money aside and saving it for whenever you have to pay for things like nanny services.

Even though the federal limit to how much you can contribute to the dependent care account is $5,000, most employers set their limits a lot lower than that. Remember, however, that the money is not transferable. So, if you contribute $5,000 and only use $3,000 on childcare during the year, your deduction will only be $3,000. The remaining $2,000 will be lost. Also, beware of a common myth that you must choose between a traditional childcare credit and an employee benefit plan. These types of claims are untrue as you could qualify for both.

Doing so, however, is quite complicated and varies on a case-by-case basis. To keep things simple and avoid any potential audits, you should switch to dependent care plans once your income puts you around the third or fourth tax bracket. This will allow you to sidestep between 22% and almost 32% of taxes that you do not have to pay on contributions made to that account.

Avoid Putting Nanny Expenses on Your Schedule C

Ultimately, you should not put any of your nanny expenses on a Schedule C that reports your business income. In the past, taxpayers used to have a lot of issues with this. For instance, someone who runs a sole proprietorship and hires a nanny is doing so for work-related purposes. So, the expenditures are justified. The IRS does not, however, consider someone who is a nanny to be an essential part of your business. Their service is not directly related to the success of your venture. Hence why you should not list them on your Schedule C as doing so entitles you to unfair deductions of the payroll costs that you incurred to compensate them.

Seek Professional Help

Since taxes revolving around childcare can be extremely complicated, you should always consider reaching out to a professional who can help you answer the question; can I deduct nanny expenses on my tax return?. That way, you will further increase the likelihood of maximizing your credit while making even more favorable strategies for hiring future nannies.Get a free consultation, or get pricing on our virtual tax prep services, now.

Comments