How to Convert to an S-Corp: 4 Easy Steps

As a solo business owner, you wear a lot of hats. You not only keep your company running like a well-oiled machine, but you also have to do the accounting, inventory, and keep up with your legal obligations. Managing your taxes, specifically how to convert to an S-Corp, can be a full-time job in some circumstances.

Unfortunately, many entrepreneurs or freelancers are so busy dealing with their day-to-day demands that they forget to step back and look at the big picture, especially when it comes to saving money on their taxes. You likely know some of the ins and outs to save money as a business owner, but you may not have thought through the possibility of converting to an S-corporation.

While managing a sole proprietorship is certainly easier from a corporate formalities and establishment perspective, it might actually be costing you money in taxes every year. Making the switch could end up saving you thousands of dollars in tax obligations each year.

What Is an S-Corporation?

An S-Corporation is a tax entity that is specifically created by the IRS. An S-corp is unlike a traditional corporation or limited liability company (LLC), which are both created by state law. It still meets the definition of a corporation from a legal standpoint, but it has the benefit of being taxed differently at the federal level. Most states will also use the same taxing methods as the federal government uses, too.

While state laws affect how you form an S-corp and how it is maintained, the IRS has its own definition for tax purposes. You need to follow both sets of laws if you want to maintain your S-corp.

An S-corp is a corporation that makes an election to be taxed as a “pass-through” entity. As a result, all of the income, losses, deductions, and credits flow through to the shareholders for federal tax purposes. Individual owners report all of the tax information for the S-corp on their personal income tax returns. In this way, an S-corp avoids the double taxation issues that plague traditional C-corporations.

Essentially, because it is a pass-through entity, an S-corp is taxed as a sole proprietorship would be. Read on to understand how to convert to an S-Corp.

Why Would You Switch to an S-Corp?

Making the switch to an S-corp from a sole proprietorship or a single-member LLC has tax advantages. Perhaps the most important tax benefit is that you can structure your company to decrease your overall tax obligations by taking advantage of how single-member LLC and sole proprietorship are taxed versus how S-Corp’s are taxed.

Both of these entities are pass-through entities like an S-corporation. However, you can be taxed less in an S-corp if you pay yourself differently in an S-corp.

What Are Self-Employment Taxes?

When you work for someone else, your employer automatically takes out your state and federal tax obligations, including your obligations related to Social Security and Medicare. When you are self-employed, in addition to regular income tax you are required pay social security and medicare in the form of self-employed taxes.

Today, in 2020, the self-employment tax rate is 15.3%. Of this amount, 12.4% will go to Social Security, and 2.9% will fund Medicare. This tax is only paid on the first $137,700 of self-employment income, and just 92.35% of your self-employment income is taxed, but for most people, that is all of their funds from their business venture.

What is the Self-Employment Tax Deduction?

Self-employed individuals can also deduct the “employer-equivalent” portion of your self-employment tax. That is, you can deduct the amount that the employer would have had to pay if you were employed by someone else. This deduction is half of your overall self-employment tax.

Changing Tax Obligations as an S-Corp: How Much Will I Save if I Convert to an S-Corp?

An S-corp saves money in taxes in two ways.

Income Splitting in an S-Corp

First, using an S-corp allows you to split your business income into two sections.

- Employee W2 Wage: Your wages or payroll as an employee of the S-corp

- Owner Distribution: Your dividends or profits from the company

When you pay yourself a salary from the company, you functionally become employed by the S-corp. The S-corp can expense your salary (and the taxes paid in relation to your salary) as a business expense.

In addition, you only have to pay self-employment taxes on the portion of the income that is provided to you as a salary, rather than all of the funds that you receive from the company as both salary and dividends. That means that you can significantly cut down your tax obligations.

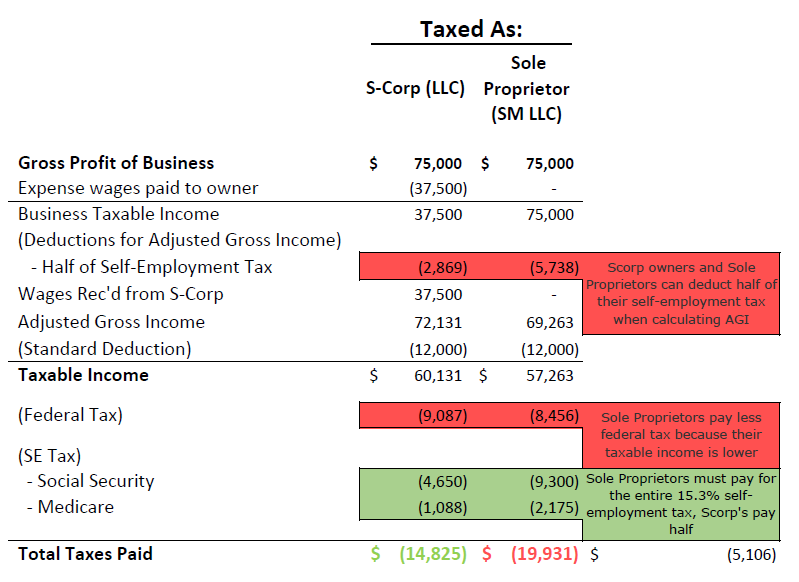

Crunching the Numbers:

In every scenario an S-Corp owner will always pay less in total taxes than a Sole Proprietor or single member LLC.

Consider the below example, where we have two self-employed individuals who’s business net profit is $75,000 per year. One is an S-Corp, and the other is either a sole proprietor or single member LLC.

You will note that the sole propripetor’s taxable income is slightly lower, which means that their federal income tax is lower as well. However when we factor in the self-employment tax effect the outcome is significantly different. The sole proprietor has to pay self-employment tax of 15.3% on the entire $75,000 in business net profit where the S-Corp only pays self-employment tax on $37,500 thus saving $5,738. The net result in the example above is that the S-Corp owner pays $5,106 less in total taxes each year. This effect is compounded as your busines’s income increases, someone earning $200,000 in business income can save over $16,000 a year in total tax just by simply converting to an S-Corp!

*INSIDER TIP* To crunch numbers to get your specific tax savings use our S-corp tax savings calculator.

By changing the structure so that you function as an employee of the S-corp, you give yourself a reasonable salary, and the remaining amount that you pay yourself is a distribution rather than income.

Owner distributions are taxed differently. In fact, they are not subject to income tax as long as the distribution does not exceed your stock basis. If it exceeds the stock basis, then the excess amount is taxed as a capital gain. In 2020, the capital gain tax rate is only up to 20% on the high end. Distributions will also completely avoid the self-employment tax that you must pay on your wages.

Steps to Convert a Sole Proprietorship or Single-Member LLC into an S-Corp

The steps on how to convert to an S-Corp for your business will vary based on whether you are currently set up as an LLC or a sole proprietorship. If you currently use a sole proprietorship, the steps will be a bit more complicated because you actually need to create an LLC first.

The steps on how to convert to an S-Corp for your business will vary based on whether you are currently set up as an LLC or a sole proprietorship. If you currently use a sole proprietorship, the steps will be a bit more complicated because you actually need to create an LLC first.

Step 1: Draft the paperwork to create an LLC

Limited liability companies are set up under state law. That means that the state where you operate your business will dictate how you should create your LLC. Generally, you will need the following documents to get you started.

- Articles of Organization

- Operating Agreement

- Employee Identification Number (EIN) by applying with the IRS)

Not every company requires an EIN, but you will use your personal Social Security Number for tax filings if you do not get an EIN. If you plan to use employees or work with independent contractors, getting EIN is a good idea so you are not sharing your personal identification information with others.

These documents can be very basic and straightforward. They will often only include fundamental information such as the company name and general contact information for the business.

Step 2: File the paperwork with the Secretary of State

You must file some or all of this paperwork with the Secretary of State in your state. Check with the Secretary of State to determine the specific information you need to register your business. Most will require that you file your Articles of Organization (sometimes called Certificate of Formation or Certification of Organization), at a minimum.

Step 3: Elect to be taxed as a Corporation

As previously mentioned, LLC’s are formed by state statute in each state and are not recognized as separate legal entities for tax purposes by the IRS. The IRS terms LLC’s as “disregarded entities” and for taxation purposes uses a default classification based on the number of owners. If the LLC has only one owner the default classification is a sole proprietorship and is required to file a Schedule C on the owners annual form 1040. If the LLC has multiple owners the the IRS default classification is a partnership and must file IRS form 1065. Fortunately, The IRS allows all LLC’s to elect to be recognized and treated as a corporation. This is a required step in creating a separate legal entity in the eyes of the IRS and is done by filing IRS form 8832.

Step 4: Elect to be taxed as an S-corp

Because making the transition to an S-corp from an LLC is a tax election rather than a legal entity change, you only need to use IRS Form 2553 to make the switch to an S-corporation. The form will require information regarding the business’s incorporation and when you want to make the transition to an S-corp.

Each shareholder of the LLC will be required to consent to make the transition to an S-corp. If you have a single-member LLC, you will be the only person that needs to approve this change.

When to Make the Switch to an S-Corp

The timing of the switch to an S-corporation is important. In some cases, if you do not file the necessary documents to elect S-corp status within a certain amount of time, you may not be able to use the election in that tax year.

- New LLCs: If you are creating an LLC for the first time, you need to submit Form 2253 within two months and 15 days from the LLC’s date of formation.

- Existing LLC: If you already had an LLC in place, you need to submit Form 2253 within two months and 15 days of the start of the tax year.

You can file Form 2253 late, but you have to have “reasonable cause” for doing so. Simply not realizing that you wanted to make the election or needed to fill out the form likely will not be enough for “cause.”

Once you have submitted Form 2253, the IRS will generally mail you an election approval letter within 45 to 60 days. Once approved, you will receive a CP261 Notice; you should keep this document with your business information.

Getting Help with the Conversion to an S-Corp

Although making the switch to an S-corp may seem like a great idea, it may not be the best option for everyone. Use our S-corp tax savings calculator to get an idea if conversion is a viable option for you. Talking to a tax professional about the implications for your unique business is a good idea, and, as the year comes to a close, now is a great time to start planning for 2021. For information on other entity options check out Money Crashers article on entity selection. You can also schedule a call with a CPA at TaxHub to talk through the pros and cons and how to convert to an S-Corp by clicking here.

Comments