Your Credit Score: 6 Things You Need To Know

If you have ever borrowed money or applied for credit, like a credit card, a credit report exists in your name. More than 180 million Americans have credit reports. That’s a lot. The thing is, many of us don’t actually know what is contained in a credit report and how that information impacts our credit scores. A little three-digit number known as your credit score can either make or break your ability to get credit. Unless you have a solid credit score, you might not be able to borrow money at a favorable rate or get access to all types of credit. There are three national credit bureaus in America: Equifax, TransUnion, and Experian. They create credit reports and credit scores with data they get about borrowers from lenders.

Answers to major questions about your credit score

Since maintaining a good score is crucial to getting access to credit, there are a few things you should know. Here are a few answers to those nagging questions you might have about your credit score:

1. How is my credit score calculated?

Credit bureaus calculate your score based on the information in your credit report. That data comes from lenders, credit bureaus, collection agencies, and other bodies. As that information is updated, your credit score might change depending upon what scoring model is being used.

2. If I close a paid-off credit card will it impact my credit score?

There isn’t a cookie-cutter answer, but generally, yes. It’s especially unwise to close out a credit card account if you’ve had it open for a long time. It might impact the average age of your accounts — another piece of information used to calculate your credit score. Lenders like to see how you handle your accounts over a period of time.

3. Should I strive for a perfect credit score?

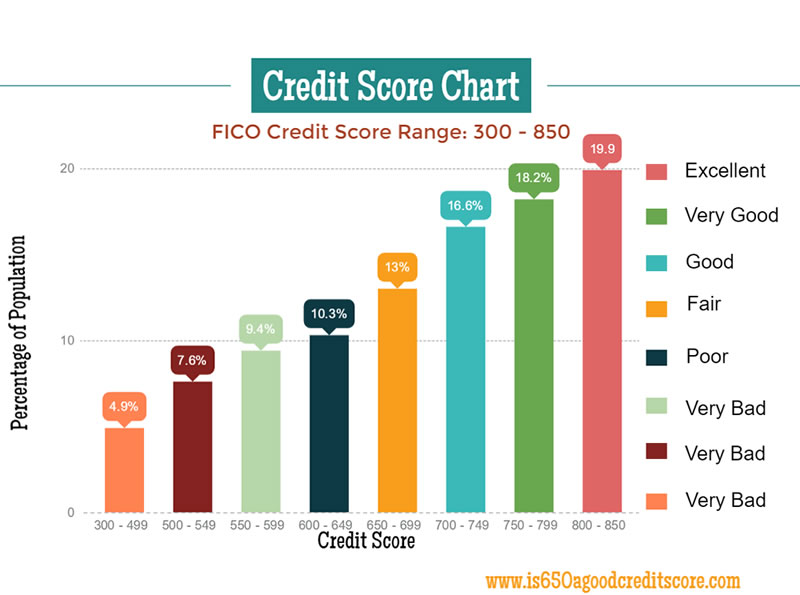

You might want to work toward a perfect score, but it might not be possible to achieve. However, scores in the 740-799 range are still considered very good, while scores 800 and above are considered excellent. Having a very good or excellent score should still give you access to good interest rates and terms. Remember though, that although there are many things you can do to improve your credit score, the process does take time. Additionally one should also consider annual fees when engaging with credit card companies

4. Why does my credit score fluctuate?

Fluctuation in credit scores is normal. Here are some reasons that might happen:

- Your payment history. Your credit score might change if you’re late on a payment or miss a payment entirely. Your payment history is one of the most important factors used to calculate your credit score, depending on what scoring model is used;

- Information changes in your credit report. Information in credit reports is always in flux since creditors, lenders, collection agencies and others, are reporting information to the three credit bureaus at all times;

- Your credit utilization. This is how much of the credit that you have access to on your credit cards and lines of credit that you’re actually using. Your credit score changes as your credit utilization changes;

- Differences in credit bureaus. Some creditors and lenders report to all credit bureaus in America, while others may report to just one or neither of them. What that means is the information these credit bureaus use to determine your credit score may be different. There are also different credit scoring models used by these bureaus and companies;

- Contrasting credit scoring models. There is more than one credit scoring model that can be used to calculate your credit score. Some of these models could be specific to a certain industry — like calculating your score for an auto loan. Your score will be different in these instances from the score you might get from the three major credit bureaus.

5. Does having a good credit score guarantee that I will get credit?

The answer to this question is no, not necessarily. There are other factors that play into the scenario such as your income, how much money or credit you’re asking for, and if it’s for a mortgage — how much of a downpayment you have.

6. Am I hopeless if I have a less than stellar credit score?

You can always work to improve your score and a bad credit score won’t necessarily impede you from ever getting access to credit. Even if you fall on hard financial times and have to declare personal bankruptcy, you can recover.

Comments